Active Versus Passive in Global Funds

Growing uncertainty in markets has rekindled the age-old “active vs. passive” debate. In 2017, PIMCO published results of an exhaustive study that showed active U.S. bond mutual funds had largely outperformed their median passive peers over many years, whereas active equity funds had not. Here we present results of a similar analysis for global bond funds distributed in Europe, Asia and Africa and ask the question: Has active fixed income management proved its worth or should investors prefer a lower-fee passive offering in the space?

For reasons discussed in our original analysis, “Bonds Are Different: Active Versus Passive Management in 12 Points ,” we come to a similar conclusion: Active global bond funds distributed in Europe, Asia and Africa have outperformed. In short: global aggregate and corporate funds consistently and significantly outperformed their passive equivalents and beat their benchmarks.Footnotei

For high yield funds, we find a more nuanced picture: Active funds outperformed available passive offerings, and both active and passive offerings significantly underperformed their respective benchmarks.

The failure of high yield funds to beat their benchmarks echoes similar findings in the U.S. and reflects the fact that, whilst bond benchmarks are not in general investible, for this asset class it is particularly the case; much of the indices are highly illiquid and exhibit, therefore, higher spreads and have correspondingly higher expected returns, all else equal.

U.S. study recap

In December of 2017, we published results of our study of the returns of active and passive fixed income and equity funds over the previous 10-year period. Figure 1 shows a high-level summary of our findings, updated to the end of 2020.

")

To summarise, we found that, in contrast with equity funds, fixed income funds in our U.S. dataset on average outperformed their equivalent median passive funds. The contrast with equities was particularly clear at more statistically meaningful, longer horizons.

Global study

We repeated the study, this time using the Morningstar Europe, Asia and Africa category for fixed income global funds.Footnoteii As with the previous U.S. study, our methods incorporated the inclusive treatment of funds that disappeared during the course of the horizon of analysis.Footnoteiii We look at this through two lenses: fund performance relative to declared benchmarks and then again relative to passive counterparts.

1. Performance versus benchmarks

Benchmark returns are challenging measures: Benchmarks are typically very broad, including a large number of highly illiquid securities; for all but the very largest managers, they are not investible. In addition, benchmarks do not reflect transaction costs for their periodic turnover. These two factors put portfolio managers benchmarked against them at a non-trivial disadvantage. As a result, we note that in Figure 2a global high yield active mandates failed to outperform their benchmarks (the same is true for passive – to an even greater extent, in fact). High yield is an asset class that in particular exhibits low liquidity in significant proportions of the index, together with high transaction costs. This puts the bar very high for funds measured against them.

")

")

Funds in both the global aggregate and global (IG) corporate categories outperformed their benchmarks for more than 50% of the fund universe over both shorter and longer horizons. In the case of global corporates, these proportions were statistically significantFootnoteiv and increased with the horizon itselfFootnotev; at the 10-year horizon, 10 out of 11 active global corporate funds outperformed their benchmarks after fees. In Figure 2b, we show the fraction of PIMCO funds in our dataset that outperformed their benchmarks and compare that with the corresponding number for non-PIMCO funds. With the exception of GIS Global High Yield Bond Fund, all PIMCO funds delivered positive alpha after fees over five-, seven- and 10-year horizons.

2. Active versus passive

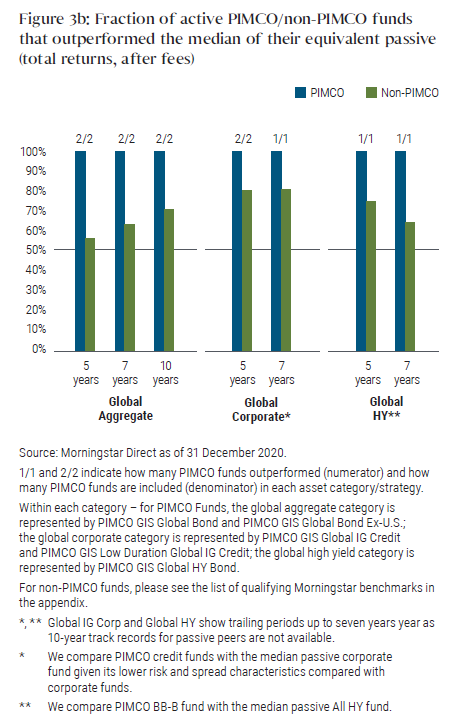

As discussed, benchmarks are not investible. In practice, the alternative to actively managed funds is to allocate to a passive fund. That being the case, arguably the most important comparison in assessing the attractiveness of active funds is to their passive counterparts. In Figure 3a we show the proportion of active funds that outperformed the median of corresponding passive funds across various time windows.

")

Once again, we see that active funds performed well, and this time that includes high yield bond funds. In all three categories, active funds historically outperformed (after fees) their median passive counterparts well over 50% of the time. We interpret this to mean that there was a significantly better-than-50% chance that an investor’s decision to go active rather than passive would have been a good one over the past 10 years. Looking at the longest available horizons, global investment grade funds would have outperformed approximately 80% of the time. For high yield, the number is lower at 64%, but still well above the crucial 50% level. Had the investor chosen to place their active allocation with PIMCO funds in these categories, all would have outperformed the medians in their categories, in terms of having beaten the passive universe median returns more than 50% of the time.

3. Why active fixed income tends to outperform

It is a widely held view – supported by empirical analyses such as our own in 2017 and 2020 – that in general active equity funds have not offered value (after fees) relative to their passive counterparts. There are several structural reasons why we nonetheless expect active bond funds to outperform passives. These include:

- A higher proportion of fixed income investors operate under constraints that create opportunities for active managers. For example, insurance companies, operating under capital constraints, eschew bonds that have been downgraded to high yield. Purchasing such “fallen angels” has provided a robust source of alpha for active managers able to add them opportunistically to their portfolios.

- Excess turnover in fixed income benchmarks creates opportunities for active bond managers:

- New securities have represented about 20% of bond market capitalisation each year.

- New issue premia enhance returns and active managers can maximize their allocations to these sources of alpha.

- Active managers can be more selective in what they buy and sell than passive funds, which have to follow the index much more closely.

- Wider availability of financial derivatives

- Compared to equity managers, fixed income managers have a larger toolbox of derivatives to fine-tune their positions to express their views in a more targeted fashion. This enhances their ability to extract value from fixed income markets, which are less efficient than equity markets due to their being less researched and more subject to noneconomic investing (see (i) above).

4. Conclusions

Our original study of U.S. fund data revealed that active bond funds in the U.S. had outperformed their passive counterparts and that equity funds had not. In this analysis of global bond funds outside of the U.S., we find similar results. Active bond funds in general beat both their benchmarks and their median passive funds over various time horizons – most crucially longer horizons where underlying skill had time to dominate the short-term noise that markets display. In all three categories – global aggregate, global (IG) corporates and global high yield – on average, investors would have chosen well had they opted for an active mandate rather than passive. Had they chosen PIMCO they would have outperformed: Morningstar data over the last 10 years indicates that 100% of PIMCO funds outperformed passive medians – far exceeding average competitor success rates. The reasons for the outperformance of active funds are many – we have listed a few – and the data is unequivocal: When it comes to fixed income, active management makes a significant difference between the two options open to bond investors.

APPENDIX

For figures 2b and 3b – the qualifying Morningstar benchmarks are below: Any base currency, hedged or unhedged

Any fund that had a prospectus benchmark in the above columns was categorised in accordance with the column header.

PLEASE ALSO NOTE:

- Only funds with passive peers were included.

- If several funds were the same except for their hedging and base currency options, we selected just one based on the following criteria:

- First, the one with the lowest fee.

- Second, (if two have the same fee level) the one with the longest history.

- For the 10-year horizon analysis we insist on a minimum of 12 months of historical data; for other horizons even one

observation is sufficient.

Featured Participants

Disclosures

For investment professionals only. PIMCO Europe Ltd (Company No. 2604517) is authorised and regulated by the Financial Conduct Authority (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. © 2022, PIMCO Europe Limited.

A company of Allianz.